In early April I spoke to the New Zealand Farm Forestry Conference in Napier about farm forestry options as I saw them. Most of the farmers I was talking to have had many years of experience in farm forestry, so I was certainly not going to tell them how to grow trees. Rather, I explored how to find a pathway through some of the challenging and at times imponderable issues that farm foresters currently face.

Many of my forestry presentations have focused on flaws in the Emission Trading Scheme (ETS). This presentation was different. I simply took the rules as they are and looked at how farm foresters could best respond in their own interests, be they economic interests or broader issues coming from the heart.

My starting point was to briefly look at the journey New Zealand’s production forestry has taken in recent decades. I used three graphs published in November 2023 in a USDA GAIM Report, where GAIN stands for Global Agricultural Information Network. GAIN reports are a great source of current and historical facts with not political messaging.

The first graph below demonstrates two key points. The lower dark-coloured area shows how New Zealand production forests were sold off in the 1990s from public to private ownership. The upper light blue area demonstrates the big uptake in forest planting in the 1990s.

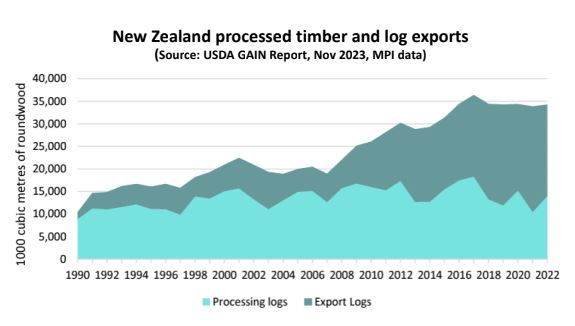

The second graph demonstrates that processed-wood volumes have bounced around but there has been no overall growth in recent years. In contrast, the log trade has grown from almost nothing thirty years ago, reaching a maximum in 2023. What the graph does not show is that export volumes are declining this year. This is not because there is less timber to be harvested, but because decreasing returns and increasing costs mean that the economics of harvesting no longer stack up on land that is steep or distant from ports.

The second graph demonstrates that processed-wood volumes have bounced around but there has been no overall growth in recent years. In contrast, the log trade has grown from almost nothing thirty years ago, reaching a maximum in 2023. What the graph does not show is that export volumes are declining this year. This is not because there is less timber to be harvested, but because decreasing returns and increasing costs mean that the economics of harvesting no longer stack up on land that is steep or distant from ports.

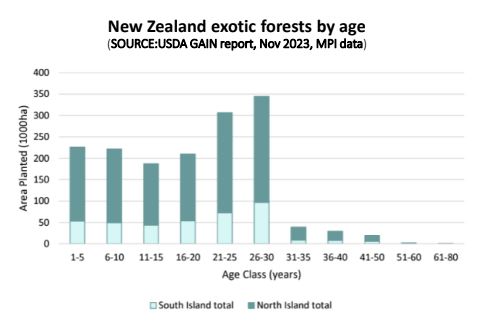

The third graph demonstrates the wall of wood aged 26 to 30 years waiting to be harvested from the big plantings in the 1990s. if it were not for economic issues that threaten harvest operations, the next five years would see more exports than ever before.

I then observed to my audience that timber is where we are more dependent on China than for any other export product, with almost 90 percent of log exports going there. I also observed that China now has less need for our timber than in the past. This is in part because China’s big infrastructure years are now behind us. Our logs are largely used for concrete formwork rather than products with higher value-add.

New Zealand is now the only country that exports significant volumes of softwood logs to China. Countries like Russia now only export lumber, not logs. Also, China is becoming increasingly self-sufficient in timber, with big eucalyptus plantings in the south of China. However, China’s timber markets are obscure and it is hard to confidently take an overall positive or negative stance about the future.

I then looked at the economics of sheep and beef farming relative to various farm-forestry options.

There is no doubt that most sheep and beef farmers are doing it tough right now. Profits in the last ten years have typically been in the range of one to two percent return on capital and slipping below that in the last three years. Right now, many farmers are cash-flow negative, with land values also dropping precipitously.

This also means that many farmers lack cash right now to convert some of the rougher country to trees.

When preparing the talk to farm foresters, I ran lots of spreadsheet models of net present values and internal rates of return for various production forestry scenarios. The big message was that using prices and costs from two to five years ago told a story of nice returns for radiata pine. But that story now belongs to history. Looking forward, the big message relating to production returns is lots of uncertainty and high economic risk.

This aligns with the current attitude of the big forestry companies. Whereas until about 18 months ago there was a mad dash to buy land for its potential timber value, that interest has disappeared. Almost no-one is interested in buying land for production timber by itself.

I then looked at what happens if land is developed out of pasture for new radiata pine production based on harvesting at 25-30 years and at the same time earning carbon credits through to 16 years under the Emission Trading Scheme (ETS)) averaging regime.

I used a conservative price of $60 per tonne of carbon (NZU) whereas the minimum prices for which the Government currently auctions carbon is $64 this year, with this price having been officially set to rise in each of the coming years.

In doing these calculations, I used the official look-up tables for radiata pine growth in different parts of New Zealand. These tables are used for assessing carbon credits for all forests of less than 100 ha and are generally considered to be conservative. Forests of more than 100 hectares are measured on actual growth.

The big message here was that carbon credits are the business to be in if converting pasture to trees. They can rapidly turn a likely unprofitable timber-production business into a profitable dual business. It did not matter what scenario I looked at, as long I used a carbon price of $60 then the internal return was acceptable, and in many cases much more than acceptable. In a typical example, it raised the IRR from around 2% to about 9% even with these low carbon prices and an inbuilt land value. It also brought the payback period including land value as a cost back to around ten years or slightly less.

These projected returns raise questions as to why the big investment companies are not doing this right now. The most important reason is that confidence has been knocked around so much over the last two years, with Governments changing the regulatory rules of the game multiple times, that commercial investors lack confidence that the rules won’t be changed again. Forestry is a long game.

I then looked at growing so-called permanent forests, where new forests are registered in the permanent scheme and then not harvested for at least 50 years. I compared this to two cycles of production timber harvested at 25 and 50 years combined with carbon credits under the averaging scheme limited to the first 16 years.

The results showed that both systems were profitable but the economics of the permanent scheme were superior under almost all realistic scenarios that I could envisage. Of course, pine forests can grow for much more than fifty years. There are radiata pines in the Wellington Botanic Gardens that are more than 160 years old. They are believed to be the first radiata pines ever brought to New Zealand

Some farm foresters are not keen on the idea of non-harvested pine forests. The reasons are generally unrelated to economics. Also, some farm foresters, who have been committed to both production and environmental forests for much of their lives, are suspicious of the whole concept of carbon farming.

Subsequent discussions went on well into the night, as we not only talked about radiata pines but also discussed eucalypts, redwoods and poplars. Within the farm forestry association there are groups of farm foresters strongly supportive of each of these other introduced species and with sound reasons developed from experience.

My own perspective is that all of these other species are underutilised within the New Zealand forestry landscape. I plan to say more about them on the coming months, and what we need to do about this.

There is also the issue of indigenous species and the role they can play. I had long discussions about this with both nursery providers and farm foresters, including the monumental issue of establishment costs. Many of the farm foresters are absolutely committed to using indigenous species, particularly for riparian plantings, but the cost of establishing indigenous woodlots at scale is so much more than for introduced species. Also, the introduced animal-pest species absolutely love indigenous trees. Introduced species are much more pest resistant.

The biggest message from all of this is that carbon credits lie at the heart of forestry economics. But it is not a simple story.

Keith Great work

You have changed/upgraded your wordpress so that one does not need to

keep on scollong down every few minutes . Also looks better

rod

as an aside, Chris Jacksons (would have been) nephew married Janettes

neice on Sat in Dunedin

Hi Rod

I have not changed anything at my end. I have not heard of that problem from others.

Keith

Hi Keith

Sorry I missed catching up e you at conf

I will try calling soon

Heading away in Wed for 2 mths to Waiheke

Things a bit hectic

Warmest best wishes

Mark

Mark Belton

Director

Emerging Forests Limited

PO Box 34, Lyttelton 8841, New Zealand

Tel: +64 (0)3 3299 203

Mob: +64 (0)27 229 1483

Email: mbelton@emergingforests.commbelton@permanentforests.com

The information contained in this email is confidential. If you are not the intended recipient, any disclosure, copying or distribution by you is prohibited and may be unlawful. If you received this e-mail by

error please advise the sender immediately by reply e-mail and delete this message and any attachments without retaining a copy.

Hi Keith

it’s not just forestry which is struggling to be economic. What percentage of dairy farmers are making a profit this year? I’d guess that 80-90% of sheep breeding properties will make a loss this financial year, or not fully maintain. When NZ’s three biggest export sectors are going backwards, it signals that some big changes are required.

NZ is living beyond its means, the government borrowing $75m per day and facing a reducing tax take. Many individuals and businesses are highly leveraged, and some will go broke. The next couple of years will be interesting, to say the least.

Wool rather than wood may come to the rescue. A recent breakthrough with deconstruction to a fine powder enables a high value product which will rescue sheep farming and promises to help close NZ’s yawning trade deficit.

warm regards

Derek Daniell

Hi Derek,

Can you point me to some info on that wool deconstruction breakthrough.

Keith

Keith, your post boldly enters NZs globally unique construct called the NZ ETS to change behaviour of the team of five million by making fossil fuels unaffordable that magically forces adoption of clean energy.

A globally unique construct to cut emissions in that it is the only country with an ETS that includes forests. But your post is not about the NZ ETS but presents direction to optimise financial gain from what the administrator MPI terms the Forestry-ETS that is synonymous with NZs ETS. MPI aid and abet via their promotions of the Forestry-ETS that forest owners can make money out of their trees and the units issued can be sold or invested, all part of a “scheme” that will apparently magically transition NZ to a low emissions economy.

On the other hand, we have a govt entity established to give parliamentarians of the day (who are not compelled to listen, that is assuming they understand) advice regarding a construct that for 15yrs has required fossil fuel distributors and so called emitters to purchase 0.48 billion tonnes of units to meet their emissions liabilities with not one tonne of behavioural emissions reduction and there never will.

The CCC proposed in their recent consultations that forests in the NZ ETS are creating ballooning (unwanted) issue of units whereby an unspecified component of registered forests be “decoupled”. It was further proposed that remaining forests be issued removal units vs NZUs and that the govt became the only purchaser at their discretion (via nationalisation), at a suggested fixed price of $35.00. I understood that the only recipient for such units would be for the free allocation of 8 million units to the trade exposed emissions intensive companies. God forbid why the team of five million should purchase $0.28 billion worth of units annually just to have them returned?

NZs post89 forest sink of 700,000 ha is a disgrace. Contrary to the MPI forecast, peak planting occurred in 1994 and peak harvest is highly likely to have occurred in 2019. If the wall of wood is still in front of us it would mean that we are surrounded by post89 plantations aged 30yrs that barely exist. The China log price booms and busts because we love to oversupply – we are well experienced at performing such a wood marketing strategy.

Approx 80% of NZs registered area of forests is owned by the corporates. I estimate that approx 60% of NZs post89 production forest estate established on ex-farm sites in the 1990s is in its second rotation.

Do you really believe that NZs construct to cut emissions will be issuing units for 50yrs? Then as per the legislation for permanent forests a roll over of two 25yr terms totaling 100yrs and to be clearfell harvested requires return of most of the units issued.

Forests are the largest contributors followed by transport emissions to NZs increasing net emissions.

In a climate crisis NZs performance to cut emissions is appalling. Our 700,000 ha post89 forest sink is appalling.

I am lost for words that in 2024 we write about how to optimise returns from the Forestry-ETS without any reference to the ineffectiveness of NZs globally unique construct to cut emissions and addressing the requirement to fix our post89, 700,000 ha forest sink.

Hi Jeff

I agree that the post 1989 forests through to about 2000 plantings have largely ‘done their dash’ in relation to sequestration, both in relation to ETS averaging and in long term reality. But sawtooth and permanents from these plantings are still relevant re the ETS.

Do you have any data to support the statement that post 89 harvest peaked in 2019. There is data to support that the total harvest reached a maximum about then. What is your opinion in relation to the third graph I presented? Do you dispute those numbers?

My own expectation is the the ETS will influence behaviours but the effects will be small unless the price of carbon increases considerably.

I remain open to the idea that a cap and tax system might be more effective than a cap and trade system. But it ain’t easy.

I am puzzled as to what you see as the path ahead.

Keith

Hi Keith

I don’t believe that sequestration wise NZs post1989 planted forest estate or sink as reported to the UN has done its dash sequestration wise. Let’s pretend the 190,000 ha Kaingaroa Forest is post1989 forest and is included in the reporting of CO2 removals from the atmosphere to the UN. It’s a carbon sink containing approx 80 million tonnes of CO2. Based on a 28yr rotation length approx 6,800 ha of forest is harvested each year and the land is replanted every year to achieve what foresters call a non-declining forest yield. Depending on how sharp the pencil is to draw the annual profile of forest sequestration, the production forest sink will “flat” line at 80,000 million tonnes in perpetuity. This forest sink would be approx equal to just one year of NZs gross emissions!

To put this pretend post1989 radiata pine, production forest sink into perspective, NZs real post1989, largely radiata pine, production forest sink is 700,000 hectares. Furthermore, it’s largely established by the large-scale corporate/TIMO growers over a ten-year period during the 1990s and early 2000s. Since this approximate 10-year planting boom, until very recently there has been no significant new land planting, instead the NZ ETS itself motivated two chainsaw massacres of pre1990 forests as quantified and reported to the UN amounting to over 200,000 ha. This area of deforestation (change of land use to agriculture) has not even been replaced by the very recent flutter of new land planting.

From a CO2 removals perspective NZs 10-year planting boom of production forests on fertile farm sites is globally unique in that it oscillates from rapid sequestration/removals to being harvested over a ten-year period or more when approx 70% of the sink is returned to the atmosphere associated with the forest harvest emissions. The tragedy for NZ is the first oscillation resulting in a mega reduction of CO2 removals occurs at the most critical time of need leading up to 2030. And to add insult to injury the second mega loss of removals occurs at the second most critical time being the lead to 2050. Unless corrected these oscillations of sequestration and harvest emissions will continue in perpetuity, even if NZ was to establish a million additional hectares of production forests.

There are some people who understand the above and believe in the lead up to 2050 we can pull the wool over the eyes of the UNFCCC as we attempted to do in the earlier days of Kyoto carbon accounting that imposed humiliation before we pulled out of the Kyoto agreement. We can apply all the make-believe domestic carbon accounting metrics we wish, but removals reported to the UN are subject to audit by (forest) engineers that understand ‘forests and land use’ defined under LULUCF, that since 2018 has been dysfunctionally absent from the MPI team that administers the so-called Forestry ETS and absent from the CCC who provide advice to parliamentarians.

May I respond to your comment regarding ETS averaging and permanent plantings. Yes, growers had the option in 2023 to swap post 2018 stands registered under default stock change accounting to averaging accounting and some growers (I don’t know why) were encouraged to take up this option. Given averaging accounting is applied via exactly the same methodology as stock change accounting for the first 16yrs (plus say 4yrs years to account for the harvested wood products component) the incorporation of averaging into reporting to the UN will be BAU through to 2043.

Regarding permanence, and the mystical plant & leave forests that Wellington based MPI staff believe is so concerning that legislation has to be drafted to protect rural landscapes from such an investment approach, for six years I have been seeking an introduction to the owner(s) of such forests that I might broaden my understanding of such an investment approach, and maybe there’s an MPI registered advisor who could also assist my education. The response to date? Silence. Thanks to Tane Mahuta that during the 1990s MAF staff did not take the same confused approach to understanding NZs new land planting boom.

Yes, I have published data that strongly indicates that peak harvest occurred in 2019. Unfortunately, subsequent years have been confounded by Covid then a series of brief price spikes followed by log price crashes and closed forest gates and yards full of contractors’ equipment. Peak harvest 2019 is supported by the math. The new land planting boom commenced in 1992, peaked in 1994 and rapidly declined by 2002. A published study showed the average harvest age on fertile farm sites with a commonly booming log price was 25 years. Age 26yrs was very uncommon and age 27yrs harvest age was almost unheard of. Harvesting down to age 21 years was also common by small forest owners particularly when contractors were on site to harvest adjacent 25yr old plantations ie harvesting was mining subsequent age classes. Peak planting in 1994 + 25yr average harvest age = peak harvest 2019. MPI forecasts assume a harvest age of 28yrs. If the peak planting year of 1994 is yet to be harvested it would infer such an age class is 30yrs old! (such a post1989 age class does not exist). I estimate that approx 60% or more of the post1989 forest estate is in its second rotation. Managed sales providers report that the remaining plantations for harvest are noticeably becoming less and less.

Keith, I’m pleased you record your expectations that you believe the NZ ETS will result in changed behaviours to cut emissions. May I evidence explain why this (economists) belief does not cut emissions and never will and why climate change is the greatest market failure the world has ever witnessed (and confounded by self-interest voluntary carbon markets).

NZ has the second highest priced packet of cigarettes globally that imposes a tax construct to make tobacco unaffordable and change behaviour to cut tobacco consumption, currently generating $2 billion and spending around $200 million annually to support stopping smoking. Analysis shows that the construct (tax) to cut tobacco use has been responsible for less than 10% of the behaviour change to quit tobacco. So, what has been responsible for this behavioural change that has resulted a reduction of people smoking to 6%? A greater awareness of the negative health outcomes from tobacco, peer pressure, legislation banning smoking in places of work including restaurants and pubs, etc.

The EU ETS is just one of four countries (x 25) that adopted an ETS as a serious construct to cut (fossil fuel power station) emissions. The EU being the worlds third largest emitter has been an outstanding success at cutting emissions (albeit focused on emissions from coal across 10,000 power stations). Early analysis shows that the EU ETS construct contributed less than 10% of the behavioural change that brought about the spectacular emissions reduction. So, what did bring about the behaviour change to cut emissions? The highly controlled market of virtual units auctioned by the EU acts as a levy on the EU team of 447 million (via power bills) generating around NZ$ 54 billion annually that is applied to cutting emissions via engineers not parliamentarians of the day.

When Minister James Shaw set up the program to get bangers off the road, subsidies for EVs and taxing utes, as per all such govt proposals the emissions reduction was from memory calculated at 10 million tonnes CO2 by 2035. The Hon Shaw sought Treasury to determine what the price of carbon would have to be to achieve an equal reduction of transport emissions. The result? Approximately $600/tonne of CO2 (compared to the current $57/tonne) that would raise the fuel emissions tax from approx 18c/litre to $1.20 with the published comment that such a price would have severe impacts on the economy and communities and also have no certainty of achieving such emissions reductions.

The only way to cut emissions is to cut emissions that also requires a levy to raise a lot of cash. Our NZ ETS has not just become broken beyond repair to cut emissions, but it was broken on 1 January 2008. The only reason it hasn’t toppled is that a CCC was dysfunctionaly appointed to provide it legitimacy. But the show/circus limps on into its 16th year whereby companies have surrendered approx 0.48 billion tonnes of CO2 with not one tonne of associated behavioural reduction of emissions and there never will.

Part of the NZ ETS dysfunction is that emissions and removals have little or nothing to do with the emissions and removals as reported by MfE to the UNFCCC. The emissions component should almost match the (Claytons) NZ ETS but it doesn’t and never will. And on the removals side MPI issued over 19 million NZUs (tonnes of CO2 removals) last year and the continuing issue of such units along with proposed emissions reductions by the CCC would almost achieve NZs 2030 reduction target that is nonsense.

You also mention a tax versus a cap & trade (construct) to cut emissions. I understand they are 50:50 in their potential outcomes. NZ has never had a cap as a component of its cap & trade construct. Even today, other than in name the NZ ETS has no cap and is downing in surplus units that will increasingly gush. NZ engages a hands free (wild west) globally unique trading scheme illustrated last year whereby the team of five million continued to be levied at the fuel pumps etc, but so-called emitters did not purchase one tonne of virtual units from the govt auctions that demonstrates the failure of the NZ ETS.

By the way, referencing a carbon price of $60 based on the govt auctions of virtual units (that is the critical basis of a successful ETS) has little or no relevance to the price received by forest growers reliance on the spot markets. Its complex and incorporates a very high volume of unit trading as an asset class, supporting an NZ ETS industry of around 10,000 players, globally unique to NZs ETS construct that is costing NZ immeasurable damage.

May I comment regarding your statements on NZs biggest and most valuable (and only wood market) China and why we forest growers wake up every morning and pay homage to China for the wealth they have brought to the NZ forest industry including the farm forestry rural communities amounting to many billions of dollars. When China arrived to NZ the average log price was in the $60s/m3 at wharf gate (in today’s value being approx $88/m3). Thanks to China’s unprecedented infrastructure program that poured more concrete in two years than the USA has poured in its entire history, and thanks to Russia and NZ or any other country not having any secret or surplus supply of logs China has had to pay an average of around NZ$135/m3 at wharf gate to secure such a globally unprecedented mega log supply. Such log price returns have been spectacular for our forest industry, albeit 60% of such supply has gone to form work, used once possibly twice, and burnt or discarded to land fill. China’s infrastructure build will eventually throttle back as occurred in my early career regarding Japan and Korea. When this happens (pessimists believe it’s already in train) and the average log price declines to sub $100 it will create the largest negative imposition the forest industry has ever experienced whereby much of our forest estate will become unprofitable to grow and harvest.

Finally, your query on the pathway ahead? “The only way to cut emissions is to cut emissions not using sticks but using carrots, lots of them (and not diverted to tax cuts).

https://www.linkedin.com/posts/jeff-tombleson-4767625_the-only-way-to-cut-emissions-is-to-cut-emissions-activity-7184381579811545088-Qb4A?utm_source=share&utm_medium=member_desktop

Nb. all the above is purposefully written with gross simplicity wearing my climate change mitigation hat devoid of self-interest. Incorporating detail particularly that relating to emissions and removals is almost impossible to understand and very few people if any have the interest to read or understand it.

Jeff

Thanks Keith, useful graphs.

I know several farmers who have sold over $1million of carbon units so far. A sceptic would suggest these sales are a tax on consumers, a huge wealth transfer that will make zero difference to the global climate. The ETS is then seen as an economic parasite. “Changing behaviour” can only mean a decrease in lifestyle until viable alternatives to oil based energy sources are freely available.

You use $60 as your conservative carbon price, but the price has been below that point sonsistently since the end of March. I’m not convinced there is much good will left for many NZ consumers to pay more and more for their survival requirements in the interests of global climate while countries such as China regularly commission new coal power stations.

On a different note, some of the yet to be published Soil Carbon studies are showing potential to increase soil C in the 500-600mm soil profile by 40T/C/ha/yr, a figure that far outweighs the sequestration of pine forests while still producing a protein crop. Looking at this option seriously seems much better for NZ than planting more permanent pine forests on farmland. Some tree species with better shade/alleopathic characteristics than conifers would allow the potential for farmers to ‘triple dip’, and grow and sell livestock, soil carbon, and tree carbon from the same hectare.

Waimata,

40T/C /ha/yr is a long way from any figures I have seen. It does not seem feasible. In general, crops are depletive of soil nitrogen but there are exceptions including one multi-year crop that I am working with.

Yes, the $60 I used is a little more than current secondary market prices, but the minimum auction price this year is $64 and increasing to $68 next year. Under current ETS settings, the price of carbon has to rise although there may be some volatility. Emitters have to get their NZUs from somewhere and if the auctions fail because of prices below the reserve price ( set by Government) then timber-sourced NZUs are the only other source.

KeithW